Introduction

You have done the responsible thing. You have homeowners or renters insurance to protect your property and guests. You also have auto insurance to cover you on the road. These policies are the foundation of your financial safety net. They each come with liability coverage, which is designed to protect you financially if you are found responsible for injuring someone or damaging their property. However, have you ever considered what might happen in the case of a major accident or a serious lawsuit?

What if the costs of a legal judgment against you exceed the liability limits of your standard policies? This is a frightening scenario that could put your savings, your investments, and even your future income at risk. To protect against this, there is a special type of coverage called umbrella insurance. It is a secondary layer of protection that sits over your existing policies. This guide will define what umbrella insurance is. We will also explain how it works with a practical example. Finally, we will discuss who should strongly consider this important coverage.

Defining Umbrella Insurance: A Second Layer of Safety

First, let’s establish a clear definition. Personal umbrella insurance is an optional type of insurance that provides additional liability coverage. It kicks in when the liability limits on your standard homeowners, auto, or boat insurance policies have been exhausted. It is specifically designed to protect you from major claims and lawsuits that could be financially devastating.

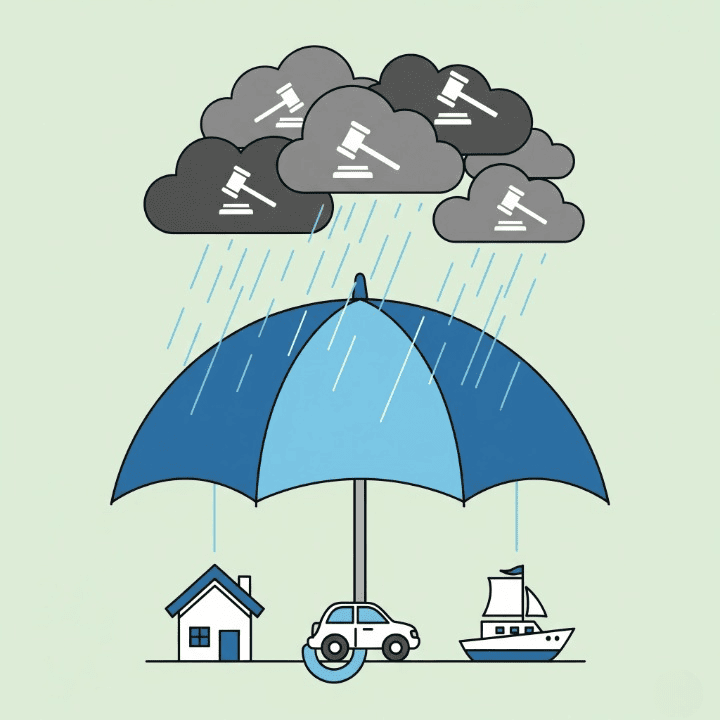

The name “umbrella” is a perfect metaphor for how this policy works.

- Think of your homeowners and auto insurance policies as your raincoat and rain boots. They are your primary gear, and they protect you from most everyday storms and showers.

- An umbrella policy, in contrast, is the large, sturdy umbrella you open up during a severe, torrential downpour.

- It provides a much broader and higher level of protection when your primary gear is overwhelmed by the severity of the storm.

It is crucial to understand that umbrella insurance is secondary coverage. It does not work on its own. To purchase an umbrella policy, insurance companies will first require you to have a certain minimum amount of liability coverage on your underlying home and auto policies. The umbrella policy only starts to pay after your primary policy’s limit has been fully paid out.

How Umbrella Insurance Works: A Real-World Scenario

The true power of an umbrella policy becomes clear with a real-world example.

Let’s imagine you have a standard auto insurance policy. The policy has a bodily injury liability limit of $300,000 per accident. In addition, you have a personal umbrella policy with a $1 million limit.

Now, imagine the worst happens. You are found at fault in a serious multi-car accident. The accident results in severe injuries to several other people. After a lengthy legal process, a court enters a judgment against you. You are found liable for a total of $800,000 to cover the other parties’ medical bills, lost wages, and pain and suffering.

Here is how your insurance policies would work together in layers:

- Your Auto Policy Pays First: Your auto insurance is your primary policy. It will pay for the damages up to its coverage limit. In this case, your auto policy pays the full $300,000.

- You Still Owe the Remainder: After your auto policy has paid its maximum, you are still legally responsible for the remaining $500,000 of the judgment.

- Your Umbrella Policy Kicks In: This is the moment your umbrella policy saves you from financial ruin. Your umbrella insurance will cover the remaining $500,000 that exceeded your auto policy’s limit.

Without the umbrella policy, you would have to pay that half-million dollars out of your own pocket. This could force you to sell your home, drain your retirement accounts, and have your future wages garnished for years. The umbrella policy provides a critical shield for your assets.

What Else Does Umbrella Insurance Cover?

Beyond simply providing higher limits, an umbrella policy often provides broader protection. It can cover certain liability claims that may be excluded from your standard home and auto policies. These can include:

- Slander: Claims against you for something you say that damages someone’s reputation.

- Libel: Claims against you for something you write that damages someone’s reputation, for example, in a negative online review.

- False Arrest or Imprisonment: Liability claims related to these situations.

- Rental Properties: It can extend your liability coverage to rental properties that you own.

- Incidents Abroad: It can often provide liability coverage when you are traveling internationally, an area where your standard U.S. auto policy might not apply.

Who Should Consider an Umbrella Policy?

While not everyone needs an umbrella policy, it is a crucial form of protection for a growing number of people. A common rule of thumb is that you should strongly consider an umbrella policy if your net worth is greater than the liability limits on your home and auto policies. Your net worth represents the assets you have that you could lose in a lawsuit.

Here are some specific groups of people who often benefit the most from this coverage:

- Homeowners. The simple act of owning property increases your potential for liability.

- People with Significant Savings or Investments. The more assets you have, the more you have to lose, and the more attractive you may be as a target for a lawsuit.

- People with “Attractive Nuisances.” This is an insurance term for things on your property that can attract children and pose a risk, such as a swimming pool, a hot tub, or a trampoline.

- High-Income Earners. Lawsuits can seek damages from both your current assets and your future earnings. High earners have more future income to protect.

- Families with Teen Drivers. Adding a young, inexperienced driver to your auto policy statistically and significantly increases your risk of being involved in a major accident.

- People who own pets. Your homeowners policy may have limited coverage for dog bites, an area where an umbrella policy can add protection.

Conclusion

In conclusion, while your standard home and auto insurance policies provide a solid and necessary foundation, an umbrella policy offers a critical next level of security. It is a relatively inexpensive layer of extra liability protection. It stands ready to safeguard your assets when a catastrophic claim exceeds the limits of your primary insurance.

In our increasingly litigious world, the importance of protecting the wealth that you have worked so hard to build cannot be overstated. An umbrella policy is one of the most cost-effective ways to shield your financial future from a single, devastating event. By taking the time to assess your own net worth and your personal risk factors, you can determine if this extra layer of protection is right for you. It is a key step in building a truly comprehensive and resilient financial plan.