Introduction

You have spent your entire working life diligently saving and investing for retirement. You have built a substantial nest egg in your 401(k)s and IRAs. Now, as you approach retirement, you face the single most important and nerve-wracking question of this new chapter: “How much of this money can I actually afford to spend each year?” The biggest fear for almost every retiree is the possibility of outliving their savings.

How do you turn a large but finite lump sum of money into a reliable, lifelong “paycheck” that can withstand the ups and downs of the stock market? To answer this exact question, the financial planning community has long relied on a famous and widely-used guideline. It is known as the 4% Rule. This simple rule of thumb provides a clear starting point for your retirement withdrawal strategy. This guide will explain what the 4% Rule is. We will also cover how it works in practice. Finally, we will discuss its modern advantages and the important limitations you need to consider.

Defining the 4% Rule: A Simple Starting Point

First, let’s establish a clear definition. The 4% Rule is a guideline for retirement withdrawals. It suggests that you can safely withdraw 4% of your total investment portfolio in your first year of retirement. After that first year, you then adjust that initial dollar amount for the rate of inflation each subsequent year. The rule is based on extensive historical data. It suggests that following this strategy provides a very high probability that your money will last for at least 30 years.

The rule was developed in the 1990s by a financial advisor named William Bengen. He conducted a study where he analyzed historical stock market and bond returns. He wanted to find the highest “safe withdrawal rate” that would have successfully survived even the worst market downturns and inflationary periods in modern history, based on a 30-year retirement timeline. His research concluded that 4% was that safe starting point.

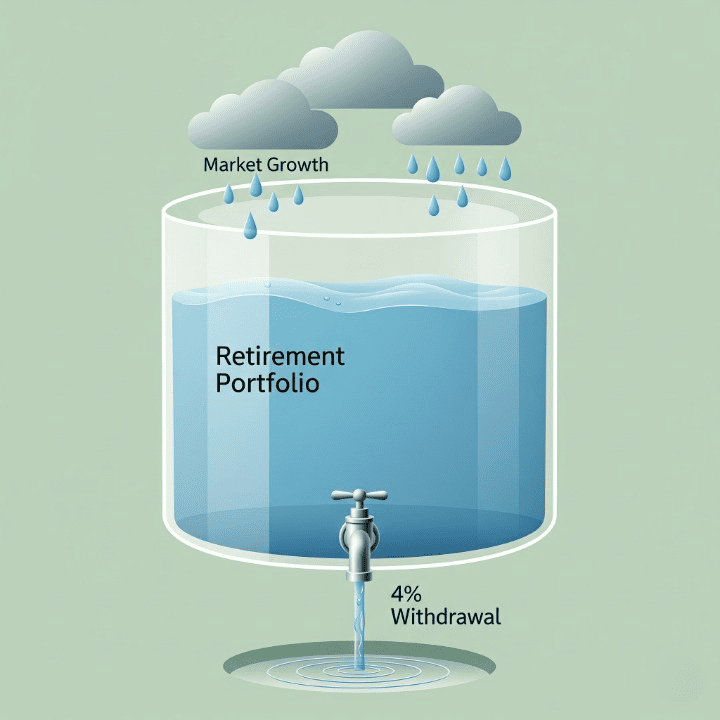

Think of your retirement portfolio with this simple analogy.

- Imagine your portfolio is a large bucket of water that you will need to drink from for the rest of your life.

- The amount of water in the bucket will naturally fluctuate. It will decrease when you take a drink (make a withdrawal), and it will be replenished by the natural rainfall (your investment returns).

- The 4% Rule is a guideline for how much water you can safely take out each year. The goal is to take out a small enough amount so that, on average, the rainfall can replenish what you take. This helps to ensure that you will not run out of water for a very long time.

How the 4% Rule Works in Practice: A Step-by-Step Example

The mechanics of the 4% Rule are straightforward, but it is crucial to understand the two-step process correctly.

Let’s look at a hypothetical retiree named Sarah. She is retiring at age 65 with a well-diversified investment portfolio worth $1,000,000.

Step 1: Calculate the First-Year Withdrawal

In her very first year of retirement, Sarah applies the 4% rule to her starting portfolio balance. $1,000,000 x 4% = $40,000 This means that in her first year of retirement, Sarah will withdraw a total of $40,000 to live on. This will be her “paycheck” for the year.

Step 2: Adjust for Inflation in All Subsequent Years

This is the most important and often misunderstood part of the rule. In year two and every year after that, you do not take out 4% of your new, current portfolio balance. Instead, you take the initial dollar amount you calculated in year one ($40,000) and you adjust it for the rate of inflation.

Let’s say that inflation during Sarah’s first year of retirement was 3%.

- To calculate her withdrawal for year two, she would increase her initial $40,000 by that 3%.

- $40,000 x 1.03 = $41,200

- In her second year of retirement, Sarah will withdraw $41,200. She will take out this amount regardless of whether her portfolio balance went up to $1.1 million or down to $900,000. She would then repeat this process every year. She would always adjust the previous year’s withdrawal amount for that year’s rate of inflation. This process is designed to help her maintain a consistent level of purchasing power throughout her retirement.

The Advantages of the 4% Rule

This rule has remained popular for decades for several good reasons.

- It is Simple and Easy to Understand. It provides a clear and concrete starting point for retirement income planning, which can be a very complex and intimidating topic.

- It Is Based on Historical Data. The rule is not just a random guess. It is based on a rigorous analysis of historical market performance. It was specifically designed to be robust enough to have survived worst-case scenarios like the Great Depression.

- It Helps Maintain Purchasing Power. The built-in annual inflation adjustment is a key feature. It helps to ensure that your retirement income can keep up with the rising cost of living over a long period.

- It Provides a Disciplined Framework. By taking out a consistent, inflation-adjusted amount each year, you avoid making emotional, market-driven decisions. It prevents you from taking out too much money during a bull market or from panic-selling too many assets during a bear market.

Modern Criticisms and Important Limitations

While the 4% Rule is an excellent guideline, it is important to understand that it is not a perfect or unbreakable law. Financial planners today often point out several important limitations.

- It Is Based on a 30-Year Retirement. The original study was designed to ensure a portfolio would last for 30 years. If you plan to retire early, for example at age 55, you will need your money to last for much longer. In this case, a more conservative withdrawal rate, such as 3% or 3.5%, might be more appropriate.

- It Is Based on Past Performance. The rule is based on historical returns of the U.S. stock and bond markets. Some economists and financial experts argue that future returns may be lower than they have been in the past. If this turns out to be true, a 4% withdrawal rate might be less safe in the future.

- It Can Be Inflexible. The rule assumes that you will want to spend the same inflation-adjusted amount every single year. However, real-life spending in retirement is often not so linear. Many retirees spend more on travel in their early, active years, and then more on healthcare in their later years. A rigid withdrawal strategy might not fit this reality.

For these reasons, most experts now agree that the 4% Rule is an excellent starting point for your retirement plan, but not necessarily the final word. It is a guideline, not a guarantee.

Conclusion

In conclusion, the 4% Rule has stood for decades as a landmark guideline in the world of retirement planning. It is a simple and effective rule of thumb. It helps to answer one of the most stressful questions that retirees face: “How much of my savings can I safely spend each year?” It provides a disciplined framework for turning your hard-earned nest egg into a reliable and sustainable income stream.

While you should be aware of its limitations and consider your own unique circumstances, the 4% Rule remains an invaluable tool. It gives you a clear and rational starting point for your calculations and for your conversations with a financial advisor. Ultimately, it helps you to confidently plan for a retirement that is not only long and happy, but also financially secure.