Introduction

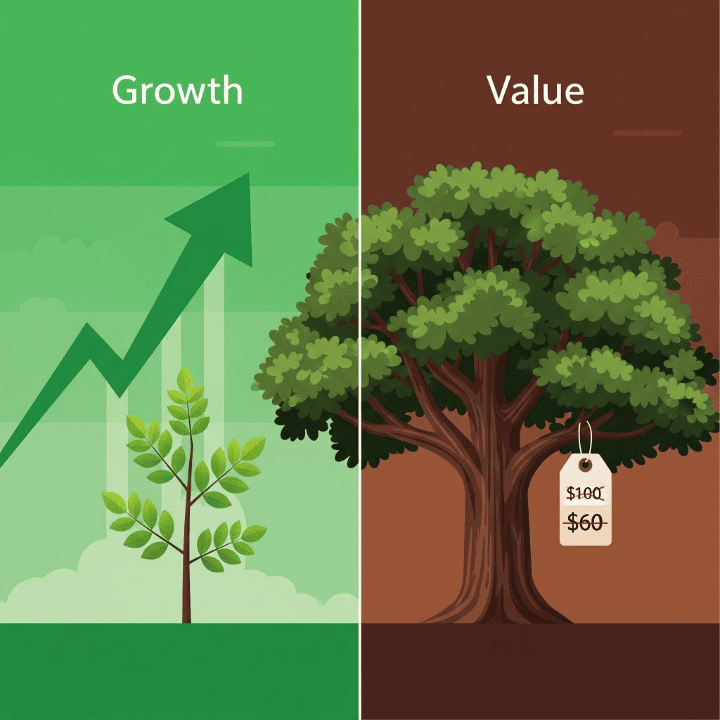

Once an investor decides to venture beyond broad market funds and into the world of individual stocks, they are faced with a universe of choices. To navigate this universe, they need a philosophy. They need a guiding principle for why a particular stock is a good investment. In the world of stock investing, two major and time-tested schools of thought have dominated this process for decades. They are growth investing and value investing.

These two approaches represent two very distinct styles for analyzing and selecting stocks. They focus on different types of companies, use different metrics for evaluation, and carry different risk profiles. One style is a hunt for the next big thing. The other is a search for hidden gems that are currently on sale. This guide will clearly define both growth and value investing. We will also explore the typical characteristics of each type of stock. Finally, we will discuss the pros and cons of each approach to help you understand these foundational investment styles.

Growth Investing: The Pursuit of Future Potential

First, let’s explore growth investing. This is an investment strategy that is focused on identifying companies that are expected to grow at a much faster rate than the overall stock market. Growth investors are often less concerned with a company’s current profitability or its stock price. Instead, they are captivated by its potential for massive future earnings and market dominance.

A great analogy for a growth investor is that of a talent scout at a high school sports competition.

- The scout is not there to watch the established, professional superstar who is already at their peak performance.

- Instead, the scout is searching for the young, athletic prodigy. This is the player who has incredible raw talent and the clear potential to become the next global superstar in their sport.

- The scout is willing to “pay up” and invest heavily in this potential, even though the young player is not yet a proven champion. In the same way, growth investors are willing to pay a premium price for a company’s stock today. They do this because they believe its future growth will more than justify that high price.

Characteristics of a Growth Stock:

- High Revenue Growth: These companies are rapidly increasing their sales, often at a rate of 20% or more per year.

- Often Unprofitable: Many growth companies are not yet profitable in a traditional sense. They are reinvesting every dollar they earn, and often more, back into the business to fund their rapid expansion, marketing, and research.

- High Valuation Metrics: Growth stocks often have very high Price-to-Earnings (P/E) ratios, or no P/E ratio at all if they are not profitable. Investors are paying a premium for their future potential, not for their current earnings.

- Innovative Industries: You can typically find these companies in innovative and fast-changing sectors of the economy. This includes industries like technology, biotechnology, or clean energy.

- The Primary Risk: The main risk of growth investing is that the expected high growth fails to materialize. If a growth company’s expansion slows down, or if it never reaches profitability, its high-flying stock price can fall dramatically.

Value Investing: The Hunt for a Bargain

Now, let’s look at the other side of the coin: value investing. This is an investment strategy that is focused on identifying good, solid companies that are trading for less than their true, intrinsic worth. Value investors are the bargain hunters of the stock market. They are looking for quality companies that are temporarily out of favor with the market for one reason or another.

The classic analogy for a value investor is that of a savvy shopper who methodically scours the clearance rack.

- This shopper is not interested in the latest, full-priced fashion trend that everyone is talking about.

- Instead, they are looking for a high-quality, well-made coat that has been marked down to 50% off. The coat might be on sale simply because it is last season’s style.

- The value investor knows that the coat is still a great, durable coat, and they are excited to buy it for less than it is actually worth.

Characteristics of a Value Stock:

- Low Valuation Metrics: Value stocks typically have low P/E ratios, low price-to-book ratios, and other financial metrics that suggest they are cheap relative to their current earnings or their underlying assets.

- Stable, Mature Businesses: They are often found in more traditional and established industries. This includes sectors like banking, insurance, consumer goods, and industrial manufacturing.

- Often Pay Dividends: Because these mature companies are not growing as rapidly, they often choose to return a portion of their consistent profits to their shareholders in the form of regular dividends.

- Temporarily Unpopular: A value stock might be cheap because its industry is in a cyclical downturn. It could also be that the company is facing a short-term, solvable problem that has caused other, more impatient investors to sell the stock.

- The Primary Risk: The main risk of value investing is the “value trap.” This is a situation where a stock appears to be cheap but is actually cheap for a very good reason. The company may have deep, fundamental problems that it can never recover from. In this case, the stock price may never bounce back.

Growth vs. Value: Two Paths to Profit

Here is a simple breakdown of the key differences between the two styles.

- Focus:

- Growth: Focuses on a company’s future potential.

- Value: Focuses on a company’s present, undervalued price.

- Typical Company:

- Growth: A young, innovative, and high-potential company.

- Value: A mature, stable, and currently out-of-favor company.

- Key Question:

- Growth: “How big can this company become?”

- Value: “How much is this company worth right now?”

Which Style Is Better?

For decades, investors have debated which style is superior. The truth is that both have proven to be successful paths to wealth creation. Each style has had long periods where it has outperformed the other. For example, value investing was the dominant style for much of the 20th century. In contrast, growth investing has been more dominant during the technology-driven era of the 21st century.

Many successful investors do not limit themselves to just one style. They may have a blended portfolio that includes both growth and value stocks. In addition, some of the very best investments are in companies that have characteristics of both. This is a strategy known as “Growth at a Reasonable Price,” or GARP.

For most individual investors, the simplest and most effective solution is to own the entire market. You can do this by investing in a broad-market index fund. This type of fund automatically holds a mix of both growth and value stocks, in proportion to their size in the market. This gives you the benefits of both styles without having to choose between them.

Conclusion

In the end, growth and value investing represent two of the most enduring and respected philosophies in the stock market. They are two different, but equally valid, ways of thinking about how to find a good investment.

Growth investors are willing to pay a premium price today for the exciting promise of a bright future. Value investors, in contrast, are patiently searching for a bargain on a solid and dependable business today. Neither style is definitively superior. Both have been proven to work over the long term, and both come with their own unique set of risks. By understanding the fundamental difference between these two investment styles, you can better interpret the strategies of professional investors. You can also gain a deeper appreciation for the different types of companies that make up the market. This knowledge is a key step in developing your own personal investment philosophy.