Introduction

You have worked hard for decades. You have diligently saved and invested in your 401(k)s and IRAs, building a nest egg for your future. Reaching retirement with a healthy portfolio is a massive achievement. However, your financial planning work is not quite finished. Many retirees are surprised to discover that their work of managing taxes continues long after they stop receiving a paycheck.

The money that you withdraw from your retirement accounts to live on is considered income. In many cases, the government will want its portion of that income. Understanding how your different sources of retirement income are taxed is a crucial part of making your money last. A smart withdrawal strategy can have a significant impact on your financial well-being. This guide will clearly explain how the most common sources of retirement income are taxed. We will cover withdrawals from retirement accounts, as well as the rules for Social Security, to help you plan for a more tax-efficient future.

The Three Buckets of Retirement Money: A Tax Framework

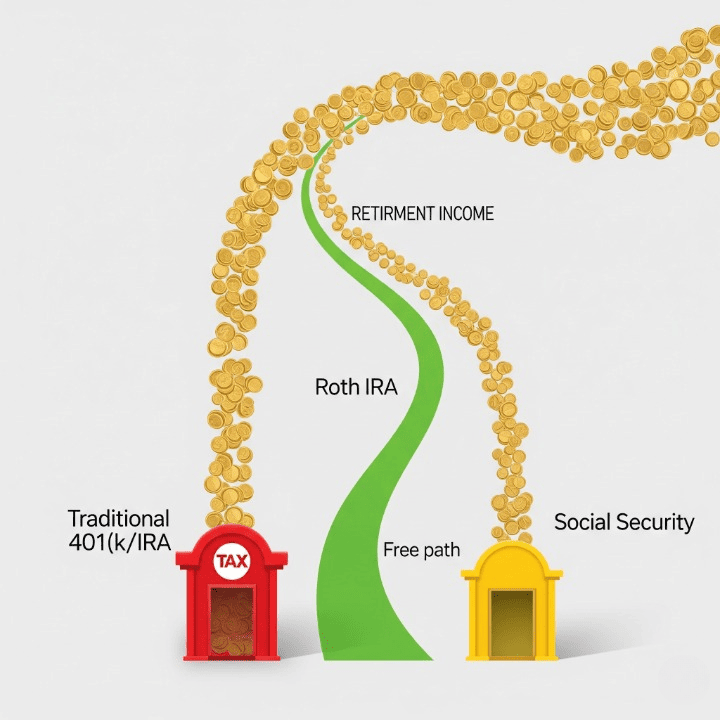

The easiest way to understand taxes in retirement is to think of your savings as being held in three different “tax buckets.” Where you saved your money during your working years will determine how it is taxed when you take it out.

Bucket 1: Tax-Deferred (Pay Taxes Later)

This bucket contains all the money that you saved on a pre-tax basis. This typically means you received an upfront tax deduction for your contributions.

- Accounts in this bucket: Traditional 401(k)s, 403(b)s, 457(b)s, Traditional IRAs, and SEP or SIMPLE IRAs.

- The Tax Rule: Every single dollar that you withdraw from these accounts in retirement is taxed as ordinary income. It will be taxed at your personal income tax rate for that year, just like a paycheck from a job would be.

Bucket 2: Tax-Free (Pay Taxes Now)

This bucket contains all the money that you saved on a post-tax basis. This means you did not receive an upfront tax deduction, as you contributed money that had already been taxed.

- Accounts in this bucket: Roth IRAs and Roth 401(k)s.

- The Tax Rule: In exchange for paying taxes on the money before you put it in, all of your qualified withdrawals in retirement are 100% tax-free. This includes both your original contributions and all the investment growth your account has earned over many decades.

Bucket 3: Taxable

This bucket contains any money you have invested in a standard, non-retirement brokerage account.

- Accounts in this bucket: Standard brokerage or investment accounts.

- The Tax Rule: You funded this account with post-tax money. Therefore, your original contributions are not taxed when you withdraw them. However, any investment growth is subject to capital gains tax when you sell the assets. Long-term capital gains tax rates are often, but not always, lower than ordinary income tax rates.

Taxes on 401(k) and Traditional IRA Withdrawals

For most retirees, the tax-deferred bucket is their largest source of retirement funds. It is essential to understand how these withdrawals are taxed. As mentioned, any money you take out of a traditional 401(k) or a traditional IRA is added to your other income for the year. It is then taxed at your marginal income tax rate.

This means that a $1 million balance in a traditional 401(k) is not actually $1 million of spending money. A significant portion of that balance is a future liability that you owe to the government in the form of taxes.

Furthermore, the government does not allow you to keep your money in these tax-deferred accounts forever. Beginning at a certain age, currently age 73, you are required by law to take out a minimum amount from these accounts each year. This is called a Required Minimum Distribution (RMD). You must take this RMD, and you must pay income tax on it, whether you actually need the money to live on or not.

The Power of Roth: Tax-Free Withdrawals

The tax-free bucket, which contains your Roth accounts, is a powerful tool in retirement. The rule is simple and beautiful. As long as you meet the qualifications (typically, your account must be at least five years old and you must be over age 59½), every single dollar you withdraw from a Roth IRA or Roth 401(k) is completely tax-free.

This tax-free money does not count as income on your tax return. This means it will not affect your tax bracket for the year. Having a source of tax-free income provides incredible flexibility in retirement. For example, if you need a large, one-time sum of money to buy a new car or to pay for a major home repair, you can pull that money from your Roth account. This action will not create a massive, unexpected tax bill for that year.

The Surprise Tax: How Social Security is Taxed

Many people are surprised to learn that their Social Security benefits may also be subject to federal income tax. Whether or not your benefits are taxed depends on your other sources of income. The government uses a formula to calculate what it calls your “combined income” or “provisional income.”

A simplified version of the formula is: Combined Income = Your Adjusted Gross Income + Nontaxable Interest + 50% of Your Social Security Benefits

Your combined income is then compared to certain thresholds.

- If your combined income is below the first threshold, your Social Security benefits are not taxed.

- If your combined income is between two thresholds, up to 50% of your Social Security benefits may be considered taxable income.

- If your combined income is above the higher threshold, up to 85% of your Social Security benefits may be considered taxable income.

This is a critical concept to understand. Large, taxable withdrawals from your traditional 401(k) or IRA can increase your combined income. This, in turn, can cause more of your Social Security benefits to become taxable. This can create a “tax-on-a-tax” situation. Withdrawals from a Roth IRA, however, do not count in the combined income formula. This is another major advantage of having tax-free funds in retirement.

Conclusion

In conclusion, your retirement planning does not end on the day you stop working. Managing your taxes in retirement is a critical component of a successful and sustainable financial plan. The decisions you make about where to withdraw your money from can have a significant impact on how long your nest egg lasts.

It is essential to remember that not all of your retirement income is treated the same by the tax authorities. Withdrawals from your traditional, tax-deferred accounts are fully taxable as ordinary income. In contrast, qualified withdrawals from your Roth accounts are completely tax-free. Even your Social Security benefits can become taxable depending on your other income sources. By understanding the different “tax buckets” where you have saved your money, you can create a smart and strategic withdrawal plan. This allows you to manage your taxable income each year, potentially reduce the taxes you pay on your Social Security benefits, and ultimately, keep more of your hard-earned money for yourself.