Introduction

Combining your life with a partner is one of the most exciting steps you can take. You build a shared home, create shared memories, and plan a shared future. A significant, and sometimes stressful, part of this process is deciding how to merge your financial lives. This is a major conversation for any serious relationship. However, there is no single rulebook for how to do it correctly.

Every couple is different. You each bring your own unique history, habits, and feelings about money to the relationship. The lack of a clear blueprint for combining your finances can lead to confusion, arguments, and missed opportunities. The goal is to build a system that feels fair and fosters a sense of teamwork. This guide will outline the three most common methods for managing money as a couple. We will explore the pros and cons of each approach. Ultimately, this will help you and your partner have a productive conversation and choose the system that works best for your unique partnership.

The Foundation: Open Communication and Shared Goals

Before we explore the different account structures, it is essential to establish the foundation upon which any successful financial partnership is built. No system will work without these three pillars.

First, you must commit to full financial transparency. The first step is to have a completely open, honest, and judgment-free conversation about money. This means putting all your cards on the table. You should share your income, your assets (savings and investments), your debts (student loans, credit cards), and even your credit scores. You should also discuss your general habits and attitudes toward money.

Second, you need to define your shared “why.” What do you, as a team, want to achieve with your money? Do you want to buy a house together in the next three years? Do you want to travel the world? Do you want to pay off all your debt and retire early? Establishing clear and exciting shared financial goals is the glue that will hold your financial partnership together. These shared goals give you a reason to work together.

Finally, you must create a joint household budget. Regardless of the account structure you choose, you need a unified plan for your combined income and expenses. This ensures that all the bills get paid and that you are both working from the same playbook.

Method 1: The “All In” Approach (Keeping It All Together)

This is the most traditional method of combining finances. In this system, both partners treat all of their income as “our money.”

- How it works: Both partners deposit their entire paychecks into one joint checking account. All household bills, from the mortgage to the groceries, are paid from this single account. All discretionary spending for both partners also comes out of this shared pot. You may also have a single joint savings account for all of your shared goals.

- Pros: This method offers the ultimate simplicity. It is very easy to track and manage your household’s cash flow. It also provides the maximum level of transparency, as both partners can see all the income and all the expenses. This can foster a strong sense of teamwork and unity.

- Cons: It can lead to a feeling of a loss of personal autonomy. Some people may feel like they have to ask their partner for permission to spend their own money. This system can also create conflict if the partners have very different spending habits.

- Best for: Couples who have similar financial habits and a strong desire for simplicity and complete financial partnership.

Method 2: The “Separate but Equal” Approach (Keeping It Apart)

This method stands on the opposite end of the spectrum. Both partners maintain their financial independence while contributing to the household.

- How it works: In this method, both partners maintain their own separate checking and savings accounts. There are no joint accounts. They work together to decide how to split the shared household bills in a way that feels fair to both of them. For example, one partner might agree to pay the rent, while the other agrees to cover the utilities and groceries. All of their personal spending money remains entirely their own.

- Pros: This system provides the maximum level of personal autonomy. You have complete control and privacy over how you choose to spend or save your own money. This can significantly reduce arguments about small, personal purchases.

- Cons: This approach can sometimes feel more like a roommate arrangement than a true financial partnership. It can make it more difficult to maintain transparency and to track your progress toward shared financial goals. It can also create feelings of inequality if there is a large income disparity between the two partners.

- Best for: Couples who place a very high value on financial independence. It is also common for couples who merge their finances later in life and who have already established their own complex financial systems.

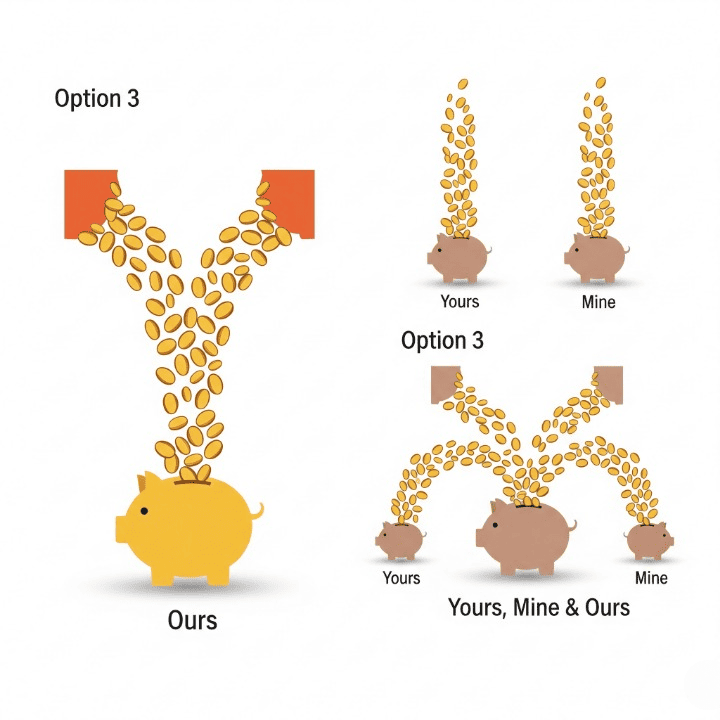

Method 3: The “Yours, Mine, and Ours” Hybrid Approach

This is an increasingly popular and balanced approach that combines the best elements of the other two methods.

- How it works: Both partners maintain their own separate checking accounts for their own personal, guilt-free spending money. In addition, they open one or more joint accounts for their shared financial life. Each partner agrees to contribute a set amount or a set percentage of their paycheck into the joint checking account each month. All of the shared household bills are then paid from this “Ours” account. They might also have a joint savings account for their shared goals, like a vacation or a house down payment.

- Pros: This is a very balanced approach. It offers both the teamwork of a joint account and the personal freedom of separate accounts. It makes managing shared expenses clear and fair, while also giving each partner the autonomy to spend their own money without judgment.

- Cons: It is slightly more complex than the “All In” method, as it requires you to manage more bank accounts.

- Best for: This hybrid approach is often the best fit for most couples. It provides a healthy balance of teamwork and independence. It is especially effective for partners who have different spending styles but still want to work together on their major financial goals.

Conclusion

In the end, there is no single “right” way for every couple to manage their money. The best system is the one that you and your partner can enthusiastically agree on. It should be a system that feels fair to both of you and that helps you work toward your shared goals with a minimum of conflict and stress.

The success of your financial partnership will depend less on the specific account structure you choose. It will depend more on your ongoing commitment to open communication, mutual respect, and your shared vision for the future. You should use these three common methods as a starting point for a conversation with your partner. Discuss what feels most comfortable for your relationship. By intentionally designing your financial system together, you can turn the challenge of merging finances into a powerful act of teamwork. This will strengthen your relationship and your financial health for years to come.