Introduction

In the world of personal finance, we spend a lot of time talking about the credit score. That important, three-digit number can have a huge impact on your life. However, your credit score is just a summary, like the final grade on a report card. The real, detailed story of your financial history is found in another, even more important document. This document is your credit report.

Your credit report is the official and comprehensive record of your history as a borrower. Lenders, landlords, insurance companies, and even some potential employers use this report to evaluate your financial responsibility. Yet, a surprising number of people have never actually seen their own credit report. They may not understand the wealth of information it contains. This guide will pull back the curtain on your credit report. We will explain what it is, break down the key sections it contains, and discuss why it is so critically important for you to review your own reports on a regular basis.

Defining the Credit Report: Your Financial History on File

First, let’s establish a clear definition. A credit report is a detailed summary of your personal history of managing credit and debt. These reports are compiled and maintained by private companies known as credit reporting agencies, or more commonly, credit bureaus. These bureaus collect financial information about you that is reported to them by the lenders and creditors you do business with. This includes banks, credit card companies, and auto finance companies.

In the United States, there are three major credit bureaus that you need to know about: Equifax, Experian, and TransUnion. Each of these bureaus maintains its own separate credit report on you. The information in your reports from all three bureaus should be very similar. However, there can sometimes be small differences. This is because some lenders may only report your account information to one or two of the bureaus, but not all three.

Think of your credit report with this simple analogy.

- Your credit score is like your final Grade Point Average (GPA) on a school transcript. It is a single, simple number that gives a quick summary of your performance.

- Your credit report, in contrast, is the full, detailed transcript. It lists every class you ever took (each of your credit accounts). It shows your grade in each of those classes (your payment history). It also lists any disciplinary actions (negative items like bankruptcies or collections). Your credit report provides the complete, detailed story of your financial habits.

The Anatomy of a Credit Report: What’s Inside?

A credit report is typically organized into five main sections. Understanding what is in each section is the key to reading your report with confidence.

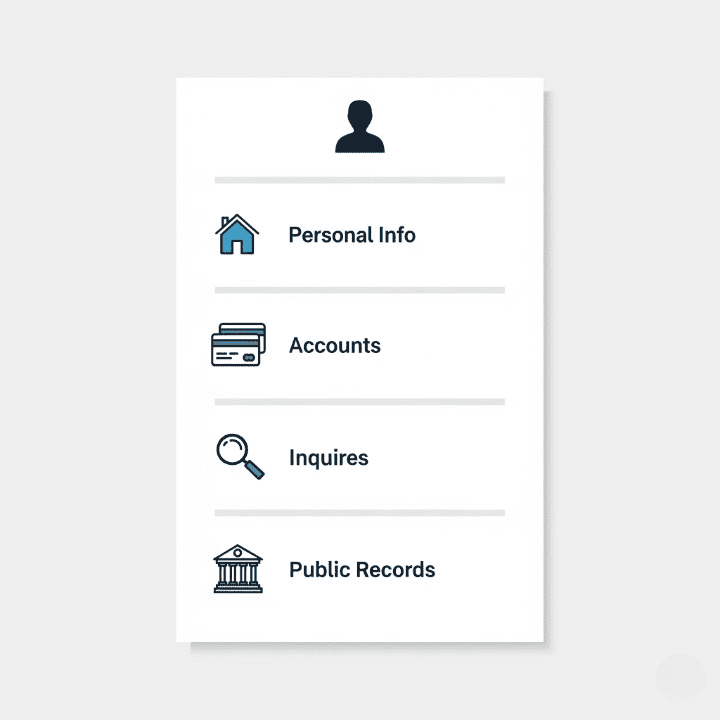

1. Personal Information

This section contains personally identifying information. It is used to confirm that the report belongs to you. This includes:

- Your full name, as well as any previous names or aliases.

- Your current and past home addresses.

- Your Social Security number.

- Your date of birth.

- Your current and past employers.

2. Credit Accounts (or “Tradelines”)

This is the heart of your credit report. It is a detailed, account-by-account list of your credit history. This includes both your open and your closed accounts. For each account, the report will typically show:

- The name of the creditor (the bank, credit union, or finance company).

- The type of account (for example, a credit card, a mortgage, or an auto loan).

- The date that you opened the account.

- Your credit limit or the original loan amount.

- The current outstanding balance on the account.

- A detailed, month-by-month payment history for the last several years, showing if you paid on time or were late.

3. Credit Inquiries

This section lists every company or entity that has accessed your credit report. There are two different types of inquiries.

- Hard Inquiries: These occur when you actively apply for new credit, such as a credit card, a loan, or a mortgage. A hard inquiry can cause your credit score to drop by a few points temporarily.

- Soft Inquiries: These occur when you check your own credit report. They also happen when a company checks your credit to send you a pre-approved offer. Soft inquiries do not affect your credit score in any way.

4. Public Records

This section contains information from public court records that is related to your finances. These items are generally considered to be very negative. They can include:

- Bankruptcies.

- Foreclosures.

- Tax liens.

5. Collections Accounts

If you have ever had a bill, such as a medical bill or a utility bill, that was so overdue that the original creditor sold the debt to a collection agency, it will appear in this section. A collections account is a serious negative item on your credit report.

Why You Must Review Your Credit Report Regularly

Reading your credit report is not just an interesting exercise. It is a critical part of maintaining your financial health. There are three main reasons why you should make a habit of it.

- To Check for Inaccuracies and Errors: Credit reports can and often do contain errors. An error could be an incorrect late payment reported by a lender. It could even be an entire account that does not belong to you. These types of inaccuracies can unfairly damage your credit score, making it harder and more expensive for you to borrow money. You have the legal right to dispute any inaccurate information you find on your credit report.

- To Spot Signs of Identity Theft: Your credit report is one of the first places that evidence of identity theft will appear. If you see a credit card or a loan account on your report that you did not open, it is a major red flag. It could mean that a criminal has stolen your personal information and is using it to open fraudulent accounts. Checking your report regularly allows you to catch this type of fraud early, before it can cause too much damage.

- To Understand Your Overall Financial Health: Your credit report provides a complete and honest picture of your relationship with debt. It can highlight the areas where you are managing your finances well. It can also show you the areas where you need to improve. It is a powerful tool for financial self-assessment.

Conclusion

In conclusion, your credit report is one of the most important and influential documents in your entire financial life. It is the detailed, official record of your history as a borrower. Furthermore, it serves as the raw data that credit scoring models use to calculate your credit score.

While your credit score is the simple summary, your credit report tells the full story. It is absolutely essential that you know what that story says about you. You should make a habit of reviewing your credit report from all three of the major credit bureaus at least once every year. By doing so, you can ensure that your financial story is being told accurately. You can protect yourself from errors and fraud. Most importantly, you can take an active and empowered role in managing your own financial reputation.