Introduction

You have likely seen the term “deductible” when getting an insurance quote. You know you have to choose a premium, which is your regular payment. Then, you see a deductible amount, often with several options like $500, $1,000, or even $2,500. Many people feel uncertain about this choice. They may not fully understand what this number truly means. Furthermore, they might not realize how it impacts their finances.

Choosing a deductible is a critical decision. In fact, it dramatically affects both your upfront cost and your potential out-of-pocket expenses after an incident. This guide will clearly explain what a deductible is. We will use practical, real-world examples to show you how it works. In addition, we will explore the crucial relationship between your deductible and your premium. Ultimately, this knowledge will help you make a much smarter decision for your financial well-being.

Defining the Deductible: Your Share of the Cost

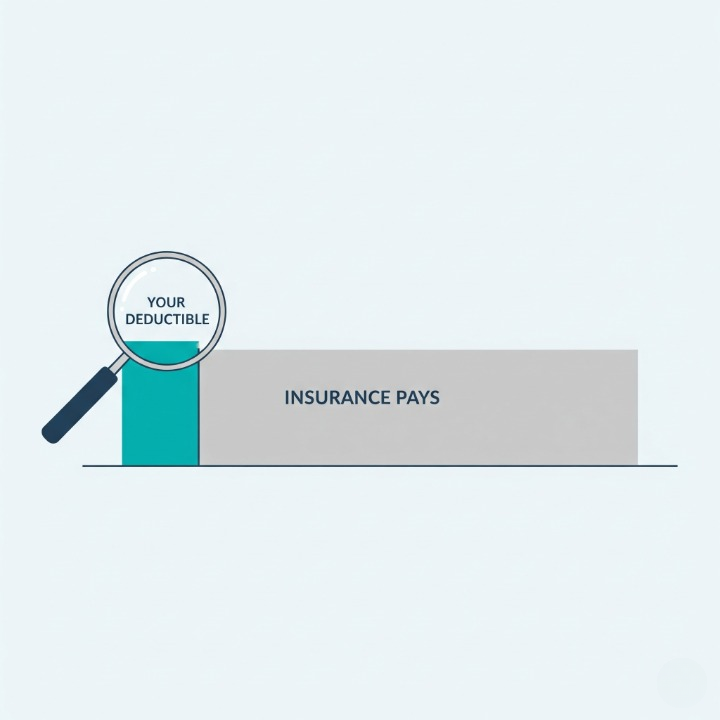

First, let’s establish a simple definition. An insurance deductible is the fixed amount of money you must pay out-of-pocket for a covered loss. Your insurance company only starts paying after you have paid this amount. In short, it is your agreed-upon share of the financial risk.

Think of your insurance policy as a cost-sharing partnership. You and your insurance company are partners. In this partnership, you agree to handle the smaller, manageable costs yourself. In return, your insurer agrees to cover the large, potentially catastrophic costs. The deductible, therefore, is the financial line that separates those small costs from the large ones.

It is also important to know when you pay a deductible. For most property insurance, like auto and home policies, you pay the deductible per claim, not per year. This means if you have two separate, unrelated car accidents in one year, you would have to meet your deductible for each claim. This differs from many health insurance plans, where the deductible is often an annual amount.

How Deductibles Work in Practice: Real-World Scenarios

The concept of a deductible becomes much clearer with real-world examples. Let’s explore a few common situations.

Scenario 1: Auto Insurance

Imagine you have a car insurance policy. Your policy includes collision coverage with a $1,000 deductible.

- Example of a Major Accident: One day, you get into an accident that causes significant damage to your car. The auto body shop gives you an estimate of $8,000 for the repairs. In this situation, your partnership with the insurer kicks in. First, you pay your $1,000 deductible directly to the repair shop. Then, your insurance company covers the rest. As a result, the insurer pays the remaining $7,000.

- Example of a Minor Accident: Now, let’s consider a different situation. You accidentally back into a pole, causing a minor dent in your bumper. The repair estimate is only $700. In this case, the total cost of the repair is less than your $1,000 deductible. Therefore, you are responsible for paying the full $700 yourself. Your insurance company would not pay anything toward this specific repair because the cost did not exceed your deductible amount.

Scenario 2: Homeowners Insurance

This same principle applies to homeowners insurance. Let’s say your policy has a $2,500 deductible.

- Example of a Covered Event: A severe hailstorm moves through your town. It causes significant damage to your roof. A contractor determines that the roof needs a full replacement, at a total cost of $15,000. To start the process, you would first pay your $2,500 deductible. After you have met your share of the cost, your insurance company will step in. Consequently, it will pay the remaining $12,500 to complete the roof replacement.

Scenario 3: Health Insurance

Health insurance deductibles usually work a bit differently. They typically apply on an annual basis.

- Example of an Annual Deductible: For instance, your health plan might have a $3,000 annual deductible. This means you must pay for the first $3,000 of most covered medical services yourself during the year. After you have paid that amount and met your deductible, your insurance plan begins to share the costs. This cost-sharing is usually done through co-pays or coinsurance for the rest of the year.

The Deductible-Premium Relationship: A Financial Balancing Act

Now we come to the most important strategic part of choosing a deductible. Your deductible has a direct and inverse relationship with your insurance premium. The rule is simple:

- A higher deductible almost always results in a lower premium.

- A lower deductible almost always results in a higher premium.

Why does this happen? The logic lies in how the insurance company views risk. When you choose a high deductible, you are agreeing to take on more potential financial risk yourself. This action demonstrates to the insurer that you are less likely to file small claims for minor damages. Because you are shouldering more of the initial risk, the insurer sees you as less of a financial risk to them. As a result, they reward you with a lower monthly or annual premium.

For example, increasing your car insurance deductible from $500 to $1,000 can often lower your premium by a noticeable amount. However, this choice has a clear consequence. You must be financially prepared to pay that higher $1,000 amount if an accident occurs.

Choosing the Right Deductible for You

There is no single “correct” deductible for everyone. The right choice is a personal financial decision that depends on your individual circumstances. Here are some key factors to consider.

First, follow the golden rule: Never choose a deductible that you cannot comfortably pay out-of-pocket tomorrow. If you do not have $2,500 readily available, you should not select a $2,500 deductible.

Second, look at your emergency fund. The size of your emergency fund is the most important factor in this decision. Your deductible should be an amount that you have set aside in savings for unexpected events. A healthy emergency fund gives you the freedom to choose a higher deductible and enjoy the lower monthly premiums.

Finally, consider your personal comfort with risk. Ask yourself a simple question. Do you prefer to pay a little more each month for the peace of mind of knowing your potential out-of-pocket cost will be low? Or, would you rather save money on your premiums each month and accept the responsibility of a higher one-time cost if something bad happens? Answering this question honestly will guide you to the right choice for you.

Conclusion

In conclusion, the deductible is a fundamental component of any insurance policy. It is not just a random number; it is a key part of the agreement you make with your insurer. It represents your share of the cost and is the amount you pay before your insurance coverage begins to pay.

Understanding the inverse relationship between your deductible and your premium is crucial. Choosing a deductible, therefore, is a deliberate balancing act. You must balance your monthly budget against your financial preparedness for an emergency. By understanding this relationship and honestly assessing your own savings, you can make a confident and informed decision. This ensures you have the protection you need without putting an unnecessary strain on your finances.