Introduction

You have made the important decision to protect your family’s future with a life insurance policy. You begin the application process. You answer questions about your lifestyle and your medical history. Then, you learn that the next step is a required medical exam. For many people, this part of the process can be a source of anxiety. They may worry about the inconvenience of the appointment. They may be concerned about what the examiner is looking for. They might even fear that a minor or unknown health issue could cause their application to be denied.

It is important to understand that the life insurance medical exam is a normal, routine, and straightforward part of the application process. It is not a scary test that you need to pass. Instead, it is simply a way for the insurance company to get a clear and accurate picture of your current health. This guide will demystify the life insurance medical exam. We will explain why it is required. We will also provide a clear, step-by-step guide of what happens during the exam. Finally, we will offer simple tips on how you can prepare to get the most accurate results possible.

The Purpose of the Exam: A Clear Picture of Your Health

The primary purpose of the life insurance medical exam is to give the insurance underwriter an objective and up-to-date snapshot of your health. This is a key part of the risk assessment process. A person who is in good health generally has a longer life expectancy. This means they represent a lower risk to the insurance company. This lower risk often translates directly into a lower and more affordable premium for the policyholder.

The medical exam serves two important functions. First, it verifies the information that you provided on your insurance application. This protects the insurance company from potential fraud. Second, it protects you as the consumer. By having a clear and verified record of your health, the insurance company can confidently and fairly price your policy. This ensures that the policy they issue to you is secure. It will be there to protect your family when they need it the most.

Think of it with this simple analogy.

- An insurance medical exam is like a home inspection that is required before you can finalize the purchase of a house.

- The inspector (the medical examiner) performs a thorough and objective check of the property’s current condition (your health).

- The buyer (the insurance company) then uses that detailed report to make a confident and fair offer (your insurance policy and premium).

What Happens During the Medical Exam? A Step-by-Step Walkthrough

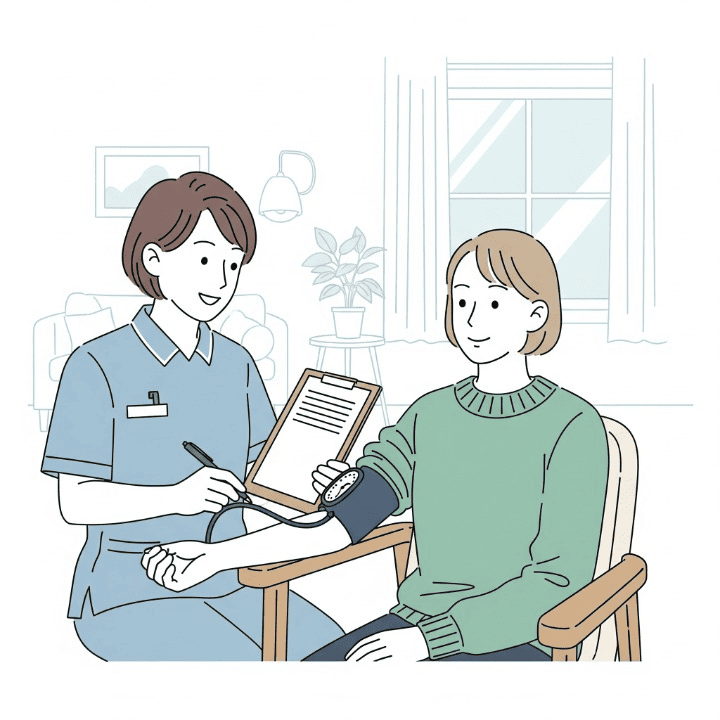

One of the most convenient aspects of the life insurance medical exam is that it is not usually conducted in a doctor’s office or a clinic. Instead, the insurance company will typically send a licensed paramedical professional to a location and a time that is convenient for you. This can be your home or even your workplace. The entire appointment is usually very quick, often taking only 20 to 30 minutes to complete.

Here is what you can typically expect during the exam:

- A Verbal Questionnaire: The examiner will begin by asking you a series of questions about your medical history. You should be prepared to discuss your personal health history, your family’s health history (parents and siblings), the names and dosages of any medications you are currently taking, and the contact information for your primary doctor. They will also ask you about your lifestyle habits, such as your use of tobacco, alcohol, or any recreational drugs.

- Basic Physical Measurements: Next, the examiner will take your basic physical measurements. This includes accurately measuring your height and weight. They will also take your blood pressure and your pulse.

- The Collection of Samples: The core of the exam is the collection of a blood sample and a urine sample. The examiner will draw a small vial of blood from your arm. They will also provide you with a container to collect a urine sample.

- Laboratory Testing: These samples are then sent to a laboratory for detailed analysis. The lab will test the samples for a wide range of things. These tests can detect nicotine and drug use. They also check for high cholesterol levels, abnormal blood sugar levels that could indicate a risk for diabetes, and certain proteins that can indicate issues with your liver or kidney function.

How to Prepare for Your Life Insurance Medical Exam

The goal of preparing for your exam is not to “trick” the test or to hide information. The goal is simply to ensure that the results provide the most accurate picture of your normal, baseline health. You want to avoid having your results skewed by your activities right before the exam.

Here are some simple tips to follow:

In the 24 Hours Before Your Exam:

- Avoid Strenuous Exercise: An intense workout can temporarily elevate your blood pressure and some of your liver enzymes. It is best to stick to light activity, like walking, for a full day before your appointment.

- Stay Well Hydrated: You should drink plenty of water in the day leading up to your exam. This can make your blood draw easier and can help to flush your system.

- Avoid Alcohol and Rich Foods: You should avoid alcohol, red meat, and foods that are high in fat or salt for at least 24 hours. These can temporarily affect your cholesterol and liver function test results.

On the Morning of Your Exam:

- Fast if Required: The insurance company will likely ask you to fast for at least 8 to 12 hours before the exam. This means you should not eat or drink anything, except for water.

- Avoid Caffeine: You should not drink coffee, tea, or caffeinated sodas on the morning of your appointment. Caffeine can cause a temporary spike in your blood pressure.

- Have Your Information Ready: To make the process go smoothly, have all your information gathered ahead of time. This includes your list of medications, your doctors’ names and addresses, and a general knowledge of your family’s medical history.

What if My Results Are Not Perfect?

Many people worry that a single, minor health issue will cause them to be denied coverage. This is usually not the case. An insurance exam is a screening tool, not a final diagnosis. A single high blood pressure reading on the day of the exam will be considered, but underwriters look at your entire health profile in context.

If you have a chronic condition, like high cholesterol or high blood pressure that is well-managed with medication, you can often still qualify for a very good rating. Underwriters are looking for evidence of well-managed and stable health. The most important thing is to be completely honest on your application from the very beginning.

Conclusion

In conclusion, the life insurance medical exam is a normal, straightforward, and important part of the process of securing meaningful life insurance coverage. It is not a test that you can pass or fail. Instead, it is a simple and convenient health screening. It provides the insurance company with the accurate information that it needs to make a fair and confident decision about your policy.

The results of this exam are a key factor that underwriters use to classify your risk and to determine your final premium. A good result that confirms your healthy lifestyle can lead to significant savings over the life of your policy. By understanding what to expect during the exam and by following a few simple preparation steps, you can eliminate any anxiety about the process. This will allow you to present the most accurate picture of your health, which will help you to secure the best possible protection for your family.