Introduction

You did everything right. You landed a great new job, and you are excited to start the next chapter of your career. In the midst of all the excitement, you receive a letter in the mail about the 401(k) account you left behind at your old company. Now you face a new set of questions. What should you do with this old account? Should you leave it there? Can you move it? Many people, unsure of what to do, simply leave it behind. Over a long career, this can create a messy trail of forgotten accounts.

Fortunately, there is a powerful and elegant solution to this problem. It is called a rollover. A rollover is a process that allows you to consolidate your old retirement savings and take direct control of your financial future. This guide will explain what a rollover is. In addition, we will cover the significant benefits of this strategy. We will also describe the different types of rollovers you can do. Finally, we will provide a clear overview of the process to empower you to make a smart decision.

Defining the Rollover IRA: Taking Control of Your Nest Egg

First, let’s be clear about the terminology. A rollover is the action of moving money from an old employer-sponsored retirement plan, like a 401(k) or 403(b), into a new retirement account. The most common destination for this money is a Rollover IRA.

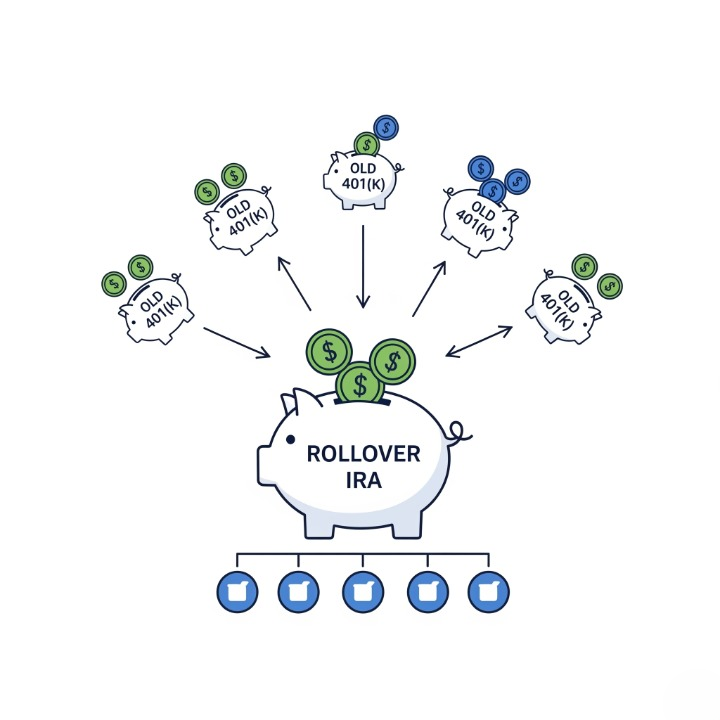

A “Rollover IRA” is not a special or distinct type of account. It is simply a Traditional IRA or a Roth IRA that you open for the specific purpose of receiving funds from your old workplace plan. Brokerage firms often label the account this way to keep the rolled-over funds separate and easily identifiable. The most important concept is that you are moving your retirement savings. You are transferring them from a plan with limited options that was managed by your old employer into a new account that you own and control completely.

Think of it with this analogy. Your old 401(k) is like a box of your valuable belongings that is being stored in the back room of your old office. A rollover is the process of moving that box to your own house, which is the IRA. Once the box is in your house, you can organize its contents however you want. You can also easily keep track of it and combine it with your other valuables.

The Powerful Benefits of a 401(k) Rollover

Taking the step to roll over your old 401(k) offers several significant advantages.

1. Greatly Expanded Investment Choices

This is often the biggest and most compelling reason to perform a rollover. Most 401(k) plans offer a limited menu of investment options, typically 10 to 20 mutual funds selected by your employer. An IRA, in contrast, opens up a nearly limitless universe of investment choices. You have the freedom to invest in thousands of different stocks, bonds, ETFs, and mutual funds. This allows you to build a low-cost, highly diversified portfolio that is perfectly aligned with your personal financial strategy.

2. Potentially Lower Fees

Workplace retirement plans can sometimes have multiple layers of fees. These can include administrative fees, record-keeping fees, and the fees of the underlying investment funds. These costs can eat away at your returns over time. By rolling your money into a low-cost IRA at a reputable brokerage firm, you can often significantly reduce the total fees you pay. This simple action can save you tens of thousands of dollars over the course of your retirement savings journey.

3. Consolidation and Simplicity

As you move through your career, you may work for several different companies. If you leave an old 401(k) behind at each job, you can quickly end up with a scattered collection of retirement accounts. This can become a logistical nightmare. You will have multiple logins, different statements, and a portfolio that is difficult to manage as a cohesive whole. Rolling over each old 401(k) into a single IRA simplifies your financial life. It makes it much easier to track your progress, manage your overall asset allocation, and see your entire retirement picture in one place.

Direct vs. Indirect Rollover: A Crucial Distinction

When you decide to perform a rollover, you will typically have two ways to do it. The method you choose is extremely important.

The Direct Rollover (Highly Recommended)

This is the safest and most straightforward method. In a direct rollover, the money moves directly from your old 401(k) provider to your new IRA provider. You never personally touch the money. The administrator of your old plan might send a check directly to your new brokerage firm. Alternatively, they might send you a check that is made payable to the new institution “for your benefit.” Because the money is never in your personal possession, there is no tax withholding and no risk of accidentally triggering a tax event or penalty.

The Indirect Rollover (Use with Extreme Caution)

In an indirect rollover, your old 401(k) provider cuts a check made out directly to you. Here is the critical part: by law, your employer is required to withhold 20% of the amount for federal income taxes. You then have 60 days to deposit the full original amount into your new IRA. This means you must come up with that withheld 20% from your own pocket to complete the full rollover. You would then reclaim the withheld 20% when you file your taxes.

The risk is enormous. If you fail to deposit the full amount within the 60-day window, the entire withdrawal is considered a taxable distribution. In that case, you would owe ordinary income tax on the amount, plus a 10% early withdrawal penalty if you are under age 59½. This can be an incredibly costly mistake. For these reasons, the direct rollover is the recommended path for almost everyone.

A Note on Roth 401(k)s and Rollovers

The rules for rollovers are designed to keep the tax status of your money the same.

- Traditional 401(k) to Traditional IRA: This is the most common type of rollover. You are moving pre-tax money into another pre-tax account. Therefore, this is a non-taxable event.

- Roth 401(k) to Roth IRA: You are moving post-tax money into another post-tax account. This is also a non-taxable event and preserves the powerful tax-free growth and withdrawal benefits of your Roth money.

- Traditional 401(k) to Roth IRA: This is possible, but it is a taxable event known as a Roth conversion. You must pay ordinary income tax on the entire amount you convert in the year that you do it.

Conclusion

In the end, managing your retirement savings is an active, lifelong process. A rollover IRA is not a new type of account. Instead, it is a crucial strategy for consolidating your retirement funds and taking control of your financial future when you transition between jobs.

The benefits are clear. A rollover can provide you with more control, greater investment choice, and potentially lower fees, all while dramatically simplifying your financial life. By understanding the rollover process, and particularly the importance of using the direct rollover method, you can confidently gather your scattered nest eggs from previous jobs. This allows you to thoughtfully manage all of your hard-earned retirement savings in one place, building a cohesive and powerful portfolio for the years to come.