Introduction

Small businesses are the lifeblood of our economy. They provide jobs and services that enrich our communities. However, due to their size and resources, they often struggle to offer the same level of benefits as large corporations. One of the most significant challenges is providing a competitive retirement plan. The cost and administrative complexity of a traditional 401(k) can be a major barrier for a small company. This can leave many employees without an easy way to save for retirement at their workplace.

To address this exact problem, the government created the SIMPLE IRA. This plan lives up to its name. The SIMPLE IRA, which stands for Savings Incentive Match Plan for Employees, is a straightforward and lower-cost retirement plan. It is designed to make it easy for small businesses and their employees to save for the future. This guide will clearly define what a SIMPLE IRA is. We will also explain its unique contribution rules. Finally, we will explore its benefits for both employers and employees.

Defining the SIMPLE IRA: An Accessible 401(k) Alternative

First, let’s establish a clear definition. A SIMPLE IRA is a type of employer-sponsored retirement plan. It is intended for small businesses, typically those with 100 or fewer employees. It functions like a traditional IRA but allows for higher contribution limits. It also includes a mandatory contribution from the employer.

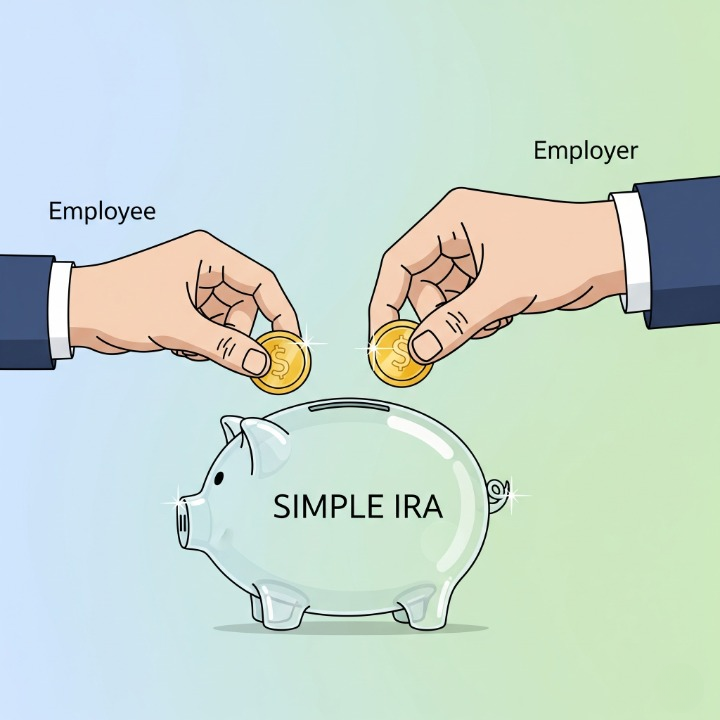

The key concept of a SIMPLE IRA is that it is a true savings partnership. It combines contributions made by the employee with a required contribution from the employer. This is a crucial difference from a 401(k) plan, where an employer match is often optional. A business that chooses to set up a SIMPLE IRA is making a firm commitment. They are required to contribute to their employees’ retirement accounts each and every year.

Think of a SIMPLE IRA like a co-op savings program for a small company.

- The employee agrees to contribute a portion of their own money from each paycheck.

- The employer, in turn, is required by the plan’s rules to put some money in alongside them, immediately boosting their savings.

- This structure creates a powerful incentive for employees to save and provides a valuable benefit that helps small businesses attract and retain talent.

How Contributions Work: The Employee and Employer Roles

The contribution structure of a SIMPLE IRA is unique. It involves both the employee and the employer in a very specific way.

The Employee Contribution

An eligible employee can choose to contribute a portion of their salary to their own SIMPLE IRA account. These contributions are made on a pre-tax basis. This means they lower the employee’s taxable income for the year. The government sets an annual limit on how much an employee can contribute. For the tax year 2025, this limit is $16,000. Employees who are age 50 or over are also allowed to make an additional “catch-up” contribution.

The Mandatory Employer Contribution

This is what makes the SIMPLE IRA plan so distinct. The employer must make a contribution to the accounts of their participating employees. They generally have two options for how to do this:

- The Matching Contribution: This is the most common choice. The employer matches the employee’s contributions dollar-for-dollar, up to a maximum of 3% of the employee’s compensation. If an employee contributes 1% of their salary, the employer matches it with 1%. If an employee contributes 3% or more of their salary, the employer contributes the full 3%. To get this match, the employee must contribute to the plan.

- The Non-elective Contribution: With this option, the employer’s contribution is not dependent on the employee’s. The employer simply contributes a flat 2% of every eligible employee’s compensation to their account. This happens whether the employee chooses to contribute to the plan or not.

Let’s look at a quick example. Maria works for a small marketing firm with a SIMPLE IRA plan. The company uses the 3% matching option.

- Maria’s annual salary is $60,000.

- She decides to contribute 5% of her salary, which is $3,000 for the year.

- Her employer then matches her contribution up to 3% of her salary. Three percent of $60,000 is $1,800.

- So, the employer contributes an additional $1,800 to Maria’s account.

- In total, Maria saves $4,800 for her retirement that year.

The Key Advantages of a SIMPLE IRA

This type of plan offers clear benefits for both small business owners and their employees.

Benefits for Employers

- Easy and Inexpensive to Administer: This is the main appeal. SIMPLE IRA plans have very simple setup procedures and minimal annual paperwork. This makes them far less burdensome and costly than a traditional 401(k).

- Tax Deductible Contributions: All contributions that the employer makes on behalf of their employees are tax-deductible as a business expense.

Benefits for Employees

- Guaranteed Employer Contribution: Unlike an optional 401(k) match, the employer contribution in a SIMPLE IRA is mandatory. This ensures that every participating employee gets a guaranteed boost to their retirement savings each year.

- 100% Immediate Vesting: An employee is always 100% vested in all money in their SIMPLE IRA account. This includes their own contributions and all contributions made by the employer. The money is theirs to keep, even if they leave the job after just a few months.

- Portability: When an employee leaves their job, the SIMPLE IRA account belongs to them. They can leave it with the current financial institution or roll it over into another IRA.

SIMPLE IRA vs. Other Plans: Where Does It Fit?

The SIMPLE IRA occupies a specific and important niche in the retirement landscape.

- Compared to a SEP IRA: A SEP IRA is funded only by the employer, and the contributions are flexible. A SIMPLE IRA involves both employee and employer contributions, and the employer’s part is mandatory. The SEP IRA allows for much higher total contributions. This often makes it a better fit for a high-income, self-employed individual. The SIMPLE IRA, in contrast, is often better for a business that wants to encourage its employees to participate in their own savings.

- Compared to a 401(k): A traditional 401(k) is more complex and expensive to run. However, it offers much higher contribution limits for both the employee and the employer. It also allows for features like plan loans, which a SIMPLE IRA does not.

The SIMPLE IRA is the perfect “starter” retirement plan. It is ideal for a small business that wants to offer a meaningful benefit but is not yet ready for the cost and complexity of a full 401(k) plan.

Conclusion

In conclusion, the SIMPLE IRA truly lives up to its name. It is a straightforward, accessible, and effective retirement plan. It is specifically designed to bridge the gap for small business owners and their employees, making it easier for them to save for a secure future. Its structure is built on a partnership. It encourages employees to save for themselves by guaranteeing that their employer will contribute alongside them.

For the millions of people who work for the small businesses that are the heart of our economy, the SIMPLE IRA provides a crucial and valuable gateway to workplace retirement saving. It proves that a powerful retirement benefit does not need to be complicated or expensive. This makes it a cornerstone of financial wellness for Main Street businesses and their dedicated staff.