Introduction

Have you ever had your budget completely derailed by a large expense that you knew was coming, but had not prepared for? This could be the annual renewal for your car insurance, the holiday season gift-buying rush, or the need to replace your worn-out tires. These are not true emergencies. They are predictable, if irregular, life expenses. Yet, for many people, they create a financial crisis. They often lead to dipping into a true emergency fund or, worse, accumulating high-interest credit card debt.

There is a simple, brilliant, and proactive strategy to handle these exact situations. It is called a sinking fund. A sinking fund is a powerful budgeting tool that turns large, intimidating future expenses into small, manageable monthly goals. This guide will clearly define what a sinking fund is. We will also explain how this strategy works. In addition, we will provide examples of what to use them for and a step-by-step guide to setting up your own.

Defining the Sinking Fund: A Targeted Savings Approach

First, let’s establish a clear definition. A sinking fund is a savings strategy. It involves setting aside a small amount of money on a regular basis, usually every month, for a specific and anticipated future expense. It is a dedicated savings pot that has only one, clearly defined job.

The core purpose of a sinking fund is to break down a large, future expense into a series of small, painless monthly savings contributions. This proactive approach allows you to accumulate the full amount of cash needed over time. As a result, when the bill finally comes due, you can pay for it in full without any stress or disruption to your regular budget.

It is crucial to understand the difference between a sinking fund and an emergency fund.

- An emergency fund is for unexpected and unplanned life crises. This includes events like a sudden job loss or an urgent medical issue.

- A sinking fund, in contrast, is for expected but irregular expenses. You know that the holidays happen every December. You know that your car will eventually need new tires. A sinking fund is the tool you use to prepare for these known future costs.

Think of it with this simple analogy. You would not take money out of your rent envelope to buy a concert ticket. Instead, you would set aside a little bit of money from each paycheck in a separate “concert” envelope. A sinking fund is just a digital version of that same, dedicated envelope strategy.

The Power of Sinking Funds: Common Examples

The beauty of the sinking fund strategy is its versatility. You can create a sinking fund for almost any large, non-monthly expense. Here are some of the most common and effective examples.

Annual or Semi-Annual Expenses

- Insurance Premiums: For car, home, or life insurance policies that you pay once or twice a year.

- Property Taxes: For homeowners who do not pay their property taxes through an escrow account.

- Subscription Renewals: For annual memberships like Amazon Prime or professional certifications.

Predictable Replacements and Maintenance

- New Tires: You know you will need to replace your tires every few years.

- Major Appliances: Your washing machine or refrigerator will not last forever. A sinking fund prepares you for its eventual replacement.

- Phone or Computer Upgrade: Saving a small amount each month for a new device.

- Car Maintenance and Repairs: For expenses like new brakes or other non-emergency repairs.

Life Events and Major Goals

- Holiday Gifts: Saving throughout the year to avoid debt in December.

- Vacations and Travel: The best way to enjoy a trip is to know it is already paid for.

- A Down Payment on Your Next Car: Saving up to pay for your next car in cash, or at least to make a very large down payment.

- Home Renovations: For planned projects like a kitchen remodel or a new deck.

How to Create Your Own Sinking Funds: A 4-Step Guide

Setting up sinking funds is a simple and empowering process.

- Identify and Prioritize Your Goals. First, make a list of all the large, irregular expenses you can anticipate for the next year or two. You might not be able to save for all of them at once. Therefore, you should prioritize the ones that are most important or are coming up the soonest.

- Determine the Target Amount and Timeline. For each goal, you need to set a clear target. How much money do you need to save, and by what date do you need it? For example, you might decide, “I need to save $1,200 for holiday gifts, and I need the money by December 1st.”

- Do the Simple Math. Next, you will divide the total target amount by the number of months you have until your deadline. This will give you your specific monthly savings goal. In our holiday example, if you start this plan in January, you have 11 months to save. So, $1,200 divided by 11 months is approximately $109 per month.

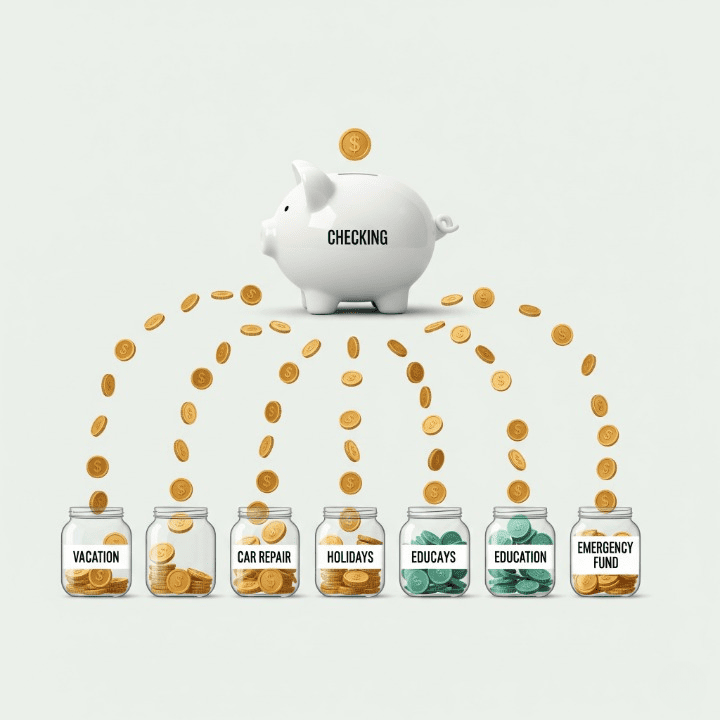

- Automate Your Savings. This is the most important step for success. The best way to manage your sinking funds is to open one or more separate savings accounts. You can then give these accounts specific nicknames, like “Vacation Fund” or “Car Repair Fund.” Finally, you should set up automatic, recurring transfers from your main checking account into these dedicated sinking funds each payday. Automation turns your good intention into a powerful and effortless habit.

The Benefits of a Sinking Fund Strategy

Adopting this strategy can have a profound and positive impact on your financial life.

- It Eliminates Financial “Emergencies.” Many of the financial crises that send people into debt are not true emergencies at all. They are simply large, unplanned-for expenses. Sinking funds transform these potential surprises into fully planned events.

- It Protects Your True Emergency Fund. By having dedicated funds for your expected expenses, you ensure that your true emergency fund is reserved only for actual, unpredictable crises like a job loss or a major medical event.

- It Reduces Financial Stress and Guilt. When you have already saved the cash for a specific purpose, you can spend it without any guilt or anxiety. This removes the stress from big purchases and allows you to truly enjoy the things you have worked hard to save for.

- It Aligns Your Spending with Your Values. The process of creating sinking funds forces you to be intentional about what is truly important to you. It helps you to proactively save for the things you value most, rather than spending money reactively.

Conclusion

In conclusion, the sinking fund is one of the most simple yet powerful tools available in personal finance. It is a proactive and highly targeted savings strategy. It prepares you in advance for the large, predictable expenses that can otherwise throw your financial life into chaos.

By breaking down your big financial goals into a series of small, automated monthly savings contributions, you can effectively eliminate the financial shocks that derail so many budgets. This allows you to pay for your significant expenses with cash, not with credit. Adopting a sinking fund strategy is a transformative step. It moves you from being a reactive spender to a proactive planner. It is a key habit that protects your emergency fund, helps you avoid debt, and gives you the freedom to spend on your goals with confidence and peace of mind.