Introduction

You have taken the crucial first step. You opened a retirement account, like a 401(k) or an IRA. Now, you face the next daunting challenge. You log in and see a list of twenty or more different investment options with confusing names. You are asked to build a diversified portfolio. How much should you put in stocks? How much in bonds? Should you invest in international markets? These questions can cause analysis paralysis. This often leads new investors to leave their money sitting in cash, earning nothing.

Fortunately, the investment industry created an elegant solution for this exact problem. It is called the Target-Date Fund (TDF). A Target-Date Fund is a simple, all-in-one investment vehicle designed to handle all the complex decisions for you. It is the definition of a “set it and forget it” strategy. This guide will explain what a Target-Date Fund is. We will also cover how its automatic adjustment feature works. Finally, we will explore the key benefits and potential drawbacks of this extremely popular retirement option.

Defining the Target-Date Fund: Investing on Autopilot

First, let’s establish a clear definition. A Target-Date Fund is a type of mutual fund that contains a diversified mix of other investment funds. It is a professionally managed portfolio wrapped up in a single, easy-to-understand product. The fund’s strategy and asset allocation are all based on a specific retirement year, which is its “target date.”

You can easily identify these funds by their names. They are almost always named with a year, such as a “Target Retirement 2050 Fund,” a “Freedom 2060 Fund,” or a “Retirement 2065 Fund.” The process for choosing one is simple. You select the fund with the year that is closest to when you plan to retire. For example, if you are 30 years old in 2025 and you plan to retire around age 70, the “Target 2065 Fund” would be an appropriate choice for you. Once you make that one choice, the fund handles the rest.

At its core, a Target-Date Fund is a “fund of funds.” The TDF itself does not buy individual stocks and bonds. Instead, it invests in a collection of other, more basic index funds. For instance, it might hold a U.S. stock index fund, an international stock index fund, and a bond index fund, all within that single TDF.

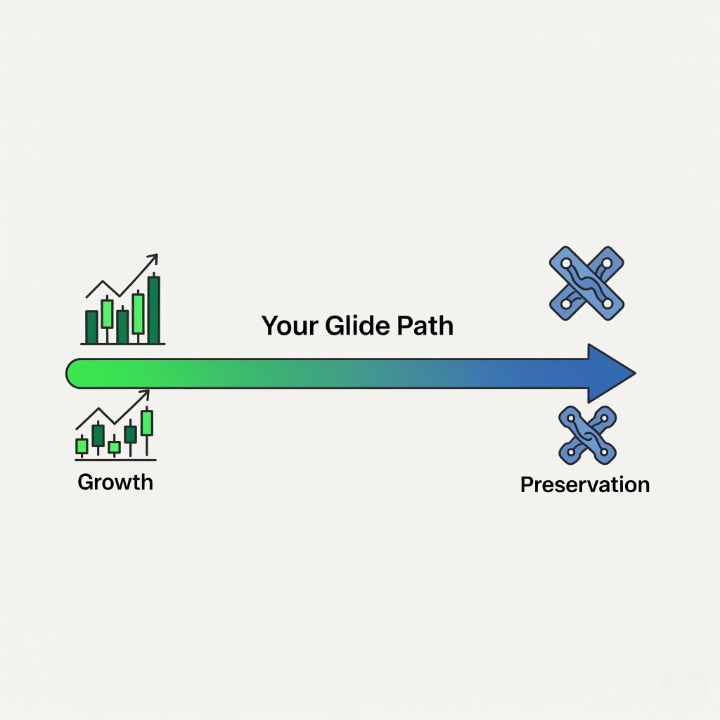

The Magic of the “Glide Path”: How TDFs Automatically Adjust

The true innovation of a Target-Date Fund is its “glide path.” This is the feature that puts your retirement savings on autopilot.

The investment philosophy is simple. A young investor with many decades until retirement can afford to take on more risk in search of higher potential growth. As that same investor gets closer to their retirement date, their priority shifts. They need to protect the wealth they have already accumulated. Therefore, their portfolio should become more conservative over time.

A glide path is the TDF’s pre-determined, gradual shift in its asset allocation. It automatically moves from a riskier allocation to a safer one as the years go by. It “glides” your portfolio toward a more conservative position as your target date approaches.

Let’s look at a hypothetical example for a “Target 2060 Fund”:

- In 2025 (35 years from retirement): A young investor chooses this fund. The fund’s asset allocation is aggressive, designed for maximum growth. It might be invested in 90% stocks and 10% bonds.

- In 2045 (15 years from retirement): The fund has been automatically and gradually adjusting itself over the past 20 years. The glide path has now shifted the mix to be more moderate. It might now be 65% stocks and 35% bonds.

- At Retirement in 2060: The fund has reached its target date. It has now glided to its most conservative allocation to protect the retiree’s capital. It might now be 50% stocks and 50% bonds.

This entire process happens automatically, behind the scenes. The investor does not have to do anything. The fund handles the slow and steady reduction of risk for them.

The Key Advantages of Target-Date Funds

The autopilot nature of TDFs provides several powerful benefits, especially for new or hands-off investors.

- Ultimate Simplicity and Convenience: This is the biggest selling point. You are only required to make one decision: choosing the fund with the correct year. After that, all the complex work of asset allocation, diversification, and rebalancing is done for you. This removes the guesswork and makes it incredibly easy to get started.

- Built-in, Broad Diversification: A single Target-Date Fund provides instant diversification across thousands of securities. It gives you exposure to U.S. stocks, international stocks, and a variety of bonds, all within one investment.

- Automatic Rebalancing: As markets fluctuate, a portfolio’s ideal mix can drift. For example, if stocks have a great year, your portfolio might become too heavily weighted in stocks. A TDF automatically rebalances its holdings for you, selling some of what has done well and buying more of what has not. This enforces a disciplined investment strategy.

- Age-Appropriate Risk Management: The glide path ensures that your investment risk is automatically tailored to your stage in life. This prevents the common mistake of being too aggressive with your investments right before you retire, or being too conservative when you are young and have a long time horizon.

Potential Drawbacks and Considerations

While TDFs are an excellent tool, it is also important to be aware of their potential downsides.

- They Are a “One-Size-Fits-All” Solution: A TDF assumes that everyone retiring in a certain year has the same tolerance for risk. Your personal risk tolerance might be higher or lower than the fund’s pre-set glide path.

- They Can Have Slightly Higher Fees: A TDF is a fund of funds, which means it has an extra layer of management. While much cheaper than most actively managed funds, TDFs often have a slightly higher expense ratio than if you were to buy the underlying index funds yourself. You are paying a small price for the convenience.

- You Have No Control Over the Allocation: Once you choose a TDF, you are handing over all asset allocation decisions to the fund manager. You cannot decide to be more heavily invested in one asset class or another. You must accept the fund’s strategy.

- All TDFs Are Not Created Equal: A “2060 Fund” from one investment company might have a different glide path, different underlying funds, and different fees than a “2060 Fund” from another company.

Conclusion

In the end, the Target-Date Fund is a remarkable innovation in the world of retirement investing. It is a simple and effective all-in-one portfolio. It is designed to remove the most common barriers that prevent people from investing for their future. The fund provides automatic diversification and a professionally managed, age-appropriate risk strategy.

The key trade-off is clear. You exchange some individual control and potentially pay slightly higher fees. In return, you receive an incredible amount of convenience and a sound, hands-off investment plan. For the millions of people who are saving for retirement through a workplace plan and want a simple, effective solution, the Target-Date Fund is an outstanding choice. It allows you to confidently start investing for your future today.