Introduction

For past generations, the idea of retirement was often built on the foundation of a traditional pension plan. It was a promise of a steady, reliable paycheck for life. Today, however, pensions are rare in the private sector. The modern retiree is now responsible for a new and daunting challenge. They must figure out how to turn their own large nest egg, saved in a 401(k) or an IRA, into a reliable income stream that can last for an unknown number of years. The fear of outliving one’s savings is one of the most significant concerns for people approaching retirement.

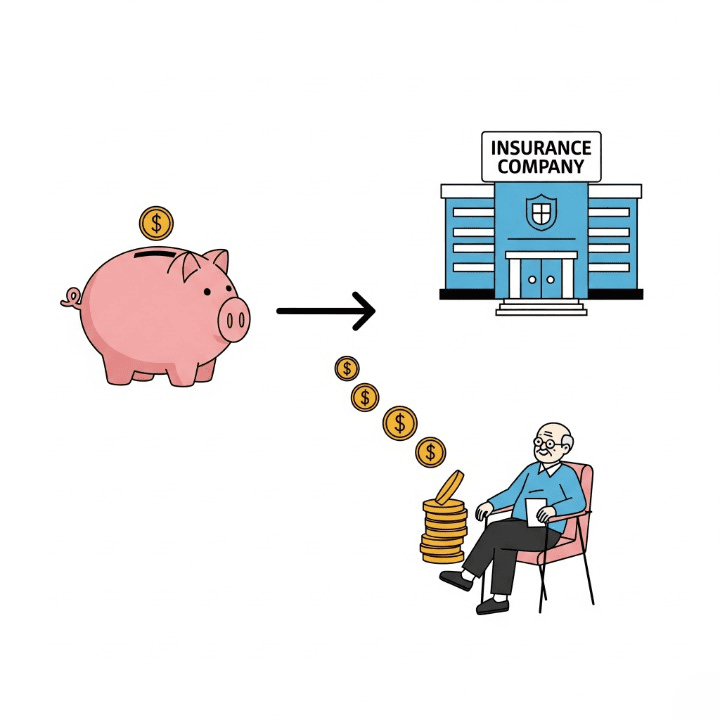

To address this exact fear, the financial industry offers a specific type of product. It is called an annuity. An annuity is a unique contract, sold by insurance companies, that is specifically designed to provide a steady and often guaranteed stream of income. This guide will clearly define what an annuity is. We will also explain how it works and break down the major types available. Finally, we will explore the key pros and cons of using an annuity as part of your retirement plan.

Defining the Annuity: A Contract for Income

First, let’s establish a clear definition. An annuity is a financial contract between you and an insurance company. In its simplest form, you pay the insurance company a sum of money. This can be either a single, large lump sum or a series of regular payments over time. In return for your payment, the insurance company promises to make regular income payments back to you. These payments can begin either immediately or at some point in the future.

The primary purpose of an annuity is to create a reliable and often guaranteed stream of income, typically for your retirement years. It is one of the only financial products that can be structured to provide an income that you are guaranteed not to outlive.

Think of an annuity with this simple analogy.

- An annuity is a way for you to create your own, private pension.

- You are giving a large portion of your savings to a professionally managed financial institution (the insurance company).

- In exchange for taking on the financial risk of managing that money, the company provides you with a steady, predictable “paycheck.”

- This paycheck can last for a specified period, such as 20 years, or even for the rest of your life.

The Two Main Phases of an Annuity

The lifecycle of most annuities can be broken down into two distinct phases.

- The Accumulation Phase: This is the period when you are funding the annuity. For a deferred annuity, this phase can last for many years. You make payments into the contract. The money in the contract then grows over time, typically on a tax-deferred basis. This means you do not pay taxes on the investment gains each year.

- The Annuitization Phase: This is the phase when the contract begins to make its regular payments back to you. You “annuitize” the contract. This means you are converting the lump sum of savings that you have built up into a stream of regular income payments. It is important to know that once you begin this phase, the decision is typically irreversible.

The Major Types of Annuities

Annuities come in many different forms. They are typically categorized based on when their payments begin and how their investment growth is calculated.

Based on Payout Timing

- Immediate Annuity: You purchase this type of annuity with a single, large lump sum payment. The income payments to you then begin almost immediately, usually within one year of the purchase. This type of annuity is best for people who are already in retirement and want to turn a portion of their savings into an instant, predictable income stream.

- Deferred Annuity: You typically fund this type of annuity over a longer period of time, such as during your working years. The money grows on a tax-deferred basis during the accumulation phase. The income payouts then begin at a future date that you choose, such as the day you officially retire.

Based on How the Money Grows

- Fixed Annuity: This is the simplest and most predictable type of annuity. During the accumulation phase, the insurance company guarantees you a fixed, minimum interest rate on your money. The future income payments that you receive are also fixed and predictable. This option offers safety and certainty, but typically has lower growth potential.

- Variable Annuity: With a variable annuity, you can invest your contributions into a selection of “sub-accounts.” These sub-accounts are very similar to mutual funds and can invest in stocks, bonds, and other assets. The value of your account and your future income will fluctuate based on the performance of these underlying investments. This option offers higher growth potential, but it also comes with the risk of market losses.

- Fixed Indexed Annuity: This is a more complex hybrid product. The returns it earns are linked to the performance of a specific market index, like the S&P 500. It offers some of the upside potential of the market. However, it also includes a guarantee to protect you from losses if the market falls.

The Pros and Cons of Annuities

Annuities are one of the most debated products in personal finance. They offer powerful benefits, but also come with significant drawbacks.

The Advantages

- Guaranteed Lifetime Income: This is the unique and primary benefit of an annuity. No other investment product can offer a contractually guaranteed income stream that you cannot outlive. This can provide incredible peace of mind in retirement.

- Tax-Deferred Growth: During the accumulation phase, your money grows without you having to pay taxes on the investment gains each year. This is a similar benefit to a 401(k) or a traditional IRA.

- Principal Protection: Fixed annuities offer a safe way to grow your money without any exposure to market risk.

The Disadvantages

- Complexity: Annuity contracts can be incredibly complex and difficult for the average person to understand. They are often filled with many rules, clauses, and specific conditions.

- High Fees and Commissions: Many annuities, especially variable and indexed annuities, are known for having high fees. These can include administrative fees, mortality and expense charges, and commissions for the salesperson. These costs can significantly reduce your overall investment returns.

- Lack of Liquidity: Your money is often locked up for a long period of time in an annuity. If you need to access your funds early, you can face steep surrender charges, which are penalties for early withdrawal.

- Lower Potential Returns: The guaranteed safety and income of a fixed annuity comes at a cost. That cost is typically lower long-term growth potential when compared to investing directly in a diversified portfolio of stocks and bonds.

Conclusion

In conclusion, the annuity is a unique and often debated tool in the world of retirement planning. It is a contract with an insurance company. It can convert a lump sum of your hard-earned savings into a predictable stream of income. In effect, it allows you to create your own, private pension.

The primary benefit of an annuity is the unparalleled security of a guaranteed income stream. This security can help to eliminate the fear of outliving your money. However, this benefit often comes at the cost of high fees, complexity, and a lack of liquidity for your savings. Annuities are not a good or a bad product in themselves. Instead, they are a specific tool for a specific job. For a retiree whose number one goal is income security, an annuity can be a valuable part of a comprehensive retirement plan. However, it is absolutely essential to fully understand the specific type of annuity, its costs, and its terms before making a long-term commitment.