Introduction

Juggling multiple debt payments each month can be an incredibly stressful experience. You have one payment for your student loan, another for your car loan, and several different payments for various credit cards. Each of these debts has its own due date, its own interest rate, and its own statement. Keeping track of it all can be a major challenge. It can be difficult to feel like you are making any real progress. In fact, it can often feel like you are just treading water against a current of interest charges.

For people who are feeling overwhelmed by this complexity, there is a financial strategy designed to solve this exact problem. It is called debt consolidation. This is a process that can bring simplicity and clarity back to your financial life. This guide will clearly define what debt consolidation is. We will also explore the most common methods for consolidating your debt. Finally, we will provide a balanced look at the significant benefits and the potential pitfalls of this popular strategy.

Defining Debt Consolidation: One Loan, One Payment

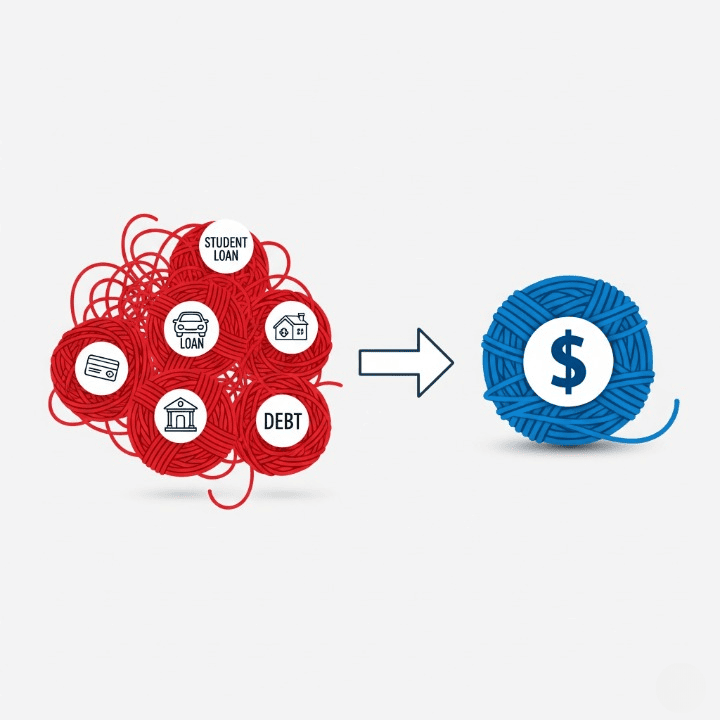

First, let’s establish a clear definition. Debt consolidation is the process of taking out a single, new loan. You then use the funds from this new loan to pay off several other, smaller debts. The primary goal is to combine multiple debt payments from various creditors into one single, predictable monthly payment. In the ideal scenario, this new, single loan will also have a lower interest rate than the average interest rate of your original debts.

It is crucial to understand what debt consolidation does and does not do. It does not magically eliminate your debt. The total amount of money you owe is still the same. Instead, you are simply reorganizing your debt. You are trading many small, often high-interest and complex debts for one larger, more manageable, and hopefully cheaper loan.

Think of it with this simple analogy.

- Imagine you have five different small fires burning in your backyard. You are trying to run between them and put them out with five different small watering cans. The process is chaotic, stressful, and inefficient.

- Debt consolidation is like using a large fire hose to gather all of that water into one powerful and focused stream. You then use that single stream to methodically put out the fire. The total amount of water you need to use (your total debt) is the same. However, your method of attack is now far more organized and effective.

The Most Common Methods of Debt Consolidation

There are two primary financial products that people use to consolidate their debt.

1. The Debt Consolidation Loan (A Personal Loan)

This is the most straightforward method. You apply for an unsecured personal loan from a bank, a credit union, or an online lender. The loan amount you request should be large enough to pay off all the existing debts that you want to consolidate.

If the lender approves your application, you will receive a lump sum of cash. You then use this cash to immediately pay off the full balances of your high-interest credit cards and other loans. After you do this, you are left with only one fixed monthly payment for the new personal loan. This loan will have a set repayment term, typically between three and seven years. The primary goal of this strategy is to secure a lower, fixed interest rate. This can save you a significant amount of money and provide you with a clear and predictable monthly payment.

2. The Balance Transfer Credit Card

This method is specifically designed for consolidating high-interest credit card debt. It involves applying for a new credit card that offers a 0% introductory Annual Percentage Rate (APR) on balance transfers. These promotional periods often last for 12 to 21 months.

You then transfer your high-interest balances from your old credit cards onto this new card. During the long 0% APR promotional period, your entire monthly payment goes toward reducing your principal balance, not toward paying interest. This can allow you to make rapid progress on paying down your debt. However, this strategy comes with a critical warning. It is only effective if you can pay off the entire transferred balance before the introductory 0% APR period ends. After that promotional period is over, a very high standard interest rate will kick in on any remaining balance.

The Powerful Benefits of Debt Consolidation

When used correctly, debt consolidation can offer several significant benefits.

- Simplicity and Organization: This is the most immediate and noticeable benefit. You go from juggling multiple payments and different due dates each month to managing just one single payment. This can dramatically reduce your financial stress and makes your monthly budget much easier to manage.

- Potential for a Lower Interest Rate: If your credit is good enough to qualify for a consolidation loan or a balance transfer card with a lower interest rate than what you are currently paying, you can save a great deal of money. A lower interest rate means that more of your payment goes toward paying down the principal. This helps you to get out of debt faster.

- A Fixed Repayment Schedule: A personal loan for debt consolidation provides you with a clear end date for your debt. You will know the exact month and year that you will be debt-free if you make all of your payments on time. This is very different from the seemingly endless and discouraging nature of making minimum payments on credit cards.

- Potential Credit Score Improvement: The “amounts owed” category is a major factor in your credit score. By paying off your revolving credit card balances with an installment loan, you can dramatically lower your credit utilization ratio. This can often lead to a significant and positive increase in your credit score.

The Risks and Pitfalls to Avoid

Debt consolidation can be a powerful tool, but it also has potential risks if it is not handled with discipline.

The single biggest risk is that it does not solve the root problem. Debt consolidation is a tool that helps you to manage the symptoms, which is your outstanding debt. However, it does nothing to address the underlying cause, which is often the spending habits that created the debt in the first place. Without a firm commitment to a budget and a change in behavior, it is very easy for a person to run their original credit card balances right back up again. This would leave them in an even worse financial position, with a new loan payment and new credit card debt.

Conclusion

In conclusion, debt consolidation can be a powerful and effective strategy for taking back control of your finances. It simplifies your financial life. It combines multiple, complex debts into a single, manageable monthly payment, and it can often lower your overall interest rate.

However, it is crucial to remember that debt consolidation is a tool for restructuring your debt, not a magic wand for eliminating it. The success of any debt consolidation plan depends entirely on your commitment to changing the underlying spending habits that led you into debt. When it is paired with a solid budget and a firm commitment to not accumulating new high-interest debt, consolidation can be a fantastic first step. It can provide you with the breathing room, the clarity, and the motivation you need to break the cycle of debt and begin your journey toward true financial freedom.